Background: services that can be offered by EMIs

Electronic Money Institutions (EMIs)1may engage in the following activities under the relevant EU regulatory framework:

a) Issuance of Electronic Money (offered by all EMIs and can be offered by credit institutions). This service is governed by EMD2 (Directive 2009/110/EC)2and includes issuance and redemption of electronic money.

EMIs can also provide all other payment services provided under PSD2 (Directive (EU) 2015/2366) but may require additional relevant permission from their regulator when doing so in relation to scriptural (commercial bank) money.

b) Other payment services set out in Annex 1 of PSD2, including Euro Credit Transfers and Direct Debits. These services are governed by the SEPA Regulation (Regulation (EU) 260/2012) and PSD2 and include:

- provision of payment accounts which are used for the execution of payments, that are accessible for payment initiation and receipt;

- provision and execution of credit transfers (SCT/SCT Inst) and/or direct debits (SDD/SDD B2B) to Payment Service Users (PSUs).

c) Payment Initiation Services (PIS). PIS require that permission be obtained by the EMI as part of a variation of the license process.

E-money represents stored monetary value that is implemented in a range of use cases typically offered by an e-money provider within a closed-loop or three-party network, while SEPA credit transfers and direct debits can only be performed from/to payment accounts identified by IBANs, with clearing, settlement and messaging layers as defined under the EPC payment schemes.

EMIs that can/should adhere to the EPC payment schemes

There are several types of transactions offered by an EMI to its clients. To determine whether an EMI can adhere to the EPC SEPA payment schemes, it is essential to assess whether the EMI meets the eligibility criteria (section 5.4 of the schemes on Eligibility), which include offering to their PSUs payment accounts as defined under Article 4, par (12), PSD23 – and in line with the interpretation provided by the EU Court of Justice (CJEU) in case C-191/174, and whether an EMI’s payment transactions fall within the scope of the SEPA Regulation, based on Article 1, par (2), (f).

Depending on the outcome of the assessment, three main categories of EMIs can be identified:

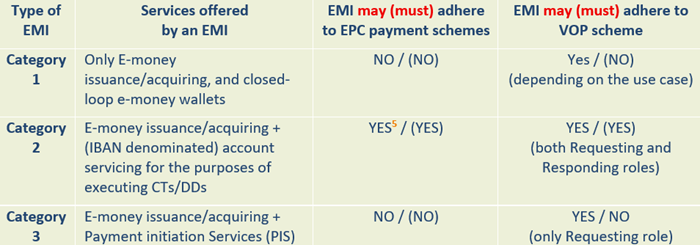

1) Category 1: EMIs not carrying out payment transactions in scope of SEPA

These EMIs typically only offer three party e-money services, allowing clients to hold e-money in wallets, transfer it to other users or merchants within the same EMI.

The accounts provided to clients in this model do not enable initiation or execution of SEPA credit transfers and direct debits from them, and the accounts held with the EMI do not meet the definition of payment account for the purposes of the EPC Scheme eligibility criteria (i.e. accounts enabling initiation and execution of SEPA credit transfers and direct debits).

Whilst such providers are subject to Titles III and IV of PSD2, the payment transactions facilitated by these EMIs are explicitly excluded from the scope of the SEPA Regulation (Article 1, par (2), (f)), and such EMIs are not eligible to participate in the EPC payment schemes.

2) Category 2: EMIs carrying out payment transactions in scope of SEPA

These EMIs offer a broader range of services including e-money issuance and IBAN-denominated4 account servicing for the purposes of executing credit transfers and/or direct debits. EMIs in this category must comply with the provisions of SEPA Regulation, as amended by the Instant Payments Regulation.

They are also subject to Titles III and IV of PSD2, which sets out requirements on transparency, execution times, consumer rights, and the requirements for obtaining direct/indirect access to the payment system. Clearing and settlement are generally facilitated through indirect access via an intermediary or a sponsor bank, but can in accordance with the provisions of the SEPA Regulation also involve direct access.

These EMIs carry out transactions that fall within the scope of the SEPA Regulation and provide clients with payment accounts enabling clients to initiate and receive SEPA credit transfers and direct debits from their account. As a result, these EMIs are eligible to and should participate in the EPC payment schemes.

3) Category 3: EMIs offering Payment Initiation Services

If an EMI does not carry out payment transactions in scope of SEPA, but is duly authorised to provide Payment Initiation Services (PIS), such an EMI could adhere to the VOP scheme as a Requesting PSP.

Adherence of EMIs to the VOP scheme

The eligibility of EMIs to adhere to the VOP Scheme is linked to the nature of payment transactions they carry out and whether those transactions fall within the scope of SEPA Regulation.

Adherence to the VOP scheme, however, has specific fraud related objectives that may extend beyond the reachability criteria for the SEPA payment schemes. In other words, the legislators recognised that it would be beneficial to payment services if the Beneficiary of a payment transaction destined to an e-money account that is not identified by an IBAN, could still be identified by the VOP scheme. This has been contemplated by the Instant Payment Regulation and implemented through the VOP scheme Rulebook, in allowing for additional means of identification. In this case, EMIs falling under Category 1 above may still decide to join the VOP scheme.

The primary criteria to determine whether or not an EMI is required to adhere to the VOP scheme is whether or not this EMI carries out or receives payment transactions in scope of SEPA Regulation.

If EMIs offer Payment Initiation Services (PIS) and provided that they are duly authorised to provide PIS under PSD2, in line with the provisions of Article 5c, par (2), amended SEPA Regulation, these EMIs must ensure that the information concerning payees they provide to the payer’s PSP is correct, and this may be achieved by adhering to the VOP scheme as Requesting PSPs.

EMIs offering only money remittance or RTGS transactions in Euro outside the SEPA framework. It may be useful to clarify that such entities may not join the Payment Scheme, nor the VOP scheme, even as a requestor only.

Annex – Overview Use Cases Table

Disclaimer

The information provided in this text is for informative purposes only and does not constitute legal advice. Payment service providers should act upon any information contained herein only after seeking professional counsel from a qualified attorney licensed in their jurisdiction to determine the schemes to which they would be required to adhere to comply with applicable law.

1As defined under Article 2 (1) of the Second Electronic Money Directive (EMD2) and included under the scope of the Second Payments Services Directive (PSD2), under Article 1(1)(a).

2 Note: EMD2 is going to be absorbed into and replaced by the forthcoming PSR and PSD3.

3 To qualify as ‘’payment account’’, an account must allow the account holder to make payments to third parties, or to receive payments from third parties.

4Note: a number of EMIs use a combination of IBAN and additional account identifiers to identify the intended Beneficiary of an incoming payment.

5 Even in case of “indirect” participation through an intermediary/sponsor bank.